To borrow a line from SEC Commissioner Daniel M. Gallagher, quoting from the fight song of his alma mater, Georgetown University: Oh How Long It’s Been!

As we approach the three year anniversary of the signing into law of the JOBS Act of 2012 it is a sad irony that many are asking: What ever became of the promise of Title III Crowdfunding and Title IV’s Regulation A+?

As we approach the three year anniversary of the signing into law of the JOBS Act of 2012 it is a sad irony that many are asking: What ever became of the promise of Title III Crowdfunding and Title IV’s Regulation A+?

At hearings held on March 10, 2015 in the U.S. Senate Committee On Banking, Housing, And Urban Affairs Subcommittee On Securities, Insurance, and Investment (a mouthful), Senators on both sides of the aisle were asking these very questions to Stephen Luparello, the Director of the SEC Division of Trading and Markets. Not surprisingly, he sidestepped the question, deferring to public remarks of SEC Chair Mary Jo White. And when Democratic Senator Mark Warner queried the Presidents of the NYSE and Nasdaq as to whether equity crowdfunding was a worthwhile endeavor for small business capital formation, essentially their answer was “Yes” – with the caveat that it needs to be properly regulated.

So with a new Republican controlled Congress in full swing, I thought this an appropriate time to take a close look at where we have come – and where we are going – as we approach the three year JOBS Act milestone – to revisit the “State of the Union” as respects the panoply of new SME capital formation tools proffered by the JOBS Act.

So with a new Republican controlled Congress in full swing, I thought this an appropriate time to take a close look at where we have come – and where we are going – as we approach the three year JOBS Act milestone – to revisit the “State of the Union” as respects the panoply of new SME capital formation tools proffered by the JOBS Act.

Title I – The IPO on Ramp

Title I – the so called “IPO On Ramp” – has made it easier for companies to stay private longer, to mitigate some of the business risks and costs inherent in the IPO process, and to reduce some of the ongoing post-IPO costs following successful completion of the IPO process. These features include:

- Allowing a company to have up to 2,000 shareholders of record (500 unaccredited) before it must become a publicly reporting company.

- Allowing a pre-IPO company to test the waters by soliciting interest before it fully commits to the time and expense of the going public process.

- Allowing a company to file its initial registration statement with the SEC on a confidential basis, thus avoiding public exposure of sensitive business data until the company determines to proceed with the offering.

- Reducing the initial and ongoing financial and non-financial disclosure during the first few years of a company’s public life.

Unlike other provisions of the JOBS Act of 2012, Title I by its terms became operational when the JOBS Act was signed into law in April 2012, requiring no SEC rulemaking for its implementation.

Unlike other provisions of the JOBS Act of 2012, Title I by its terms became operational when the JOBS Act was signed into law in April 2012, requiring no SEC rulemaking for its implementation.

By most measures Title I thus far has been a success for companies that reach a stage of development where they are able to consider accessing public capital markets. One notable beneficiary has been the Biotech industry – which for the past decade has, for the most part, been shut out of the IPO market. 2014 alone proved to be a record year for completed biotech IPO’s – undoubtedly a direct result of provisions allowing these companies to “test the waters” and to market the offering confidentiality. Thomas Farley, President of the NYSE, echoed this sentiment in his recent testimony before the Senate Subcommittee on Securities, noting that the testing the waters and confidential filing provisions have proven to be a success and even calling for their expansion.

Title II – General Solicitation in “Private” Placements to Accredited Investors

From a regulatory point of view, this legislative fix was transformational, especially in the age of the Internet, allowing a company engaged in a private placement to solicit its offering to the general public so long as the company established reasonable procedures to ensure that all of the ultimate purchasers met the traditional financial accreditation criteria – $200,000 annual income or $1 million in net worth, excluding one’s principal residence. Unlike Title I, implementation of this provision was dependent upon SEC rulemaking, with a 90 day Congressional deadline – one that came and went without final rules until September 2013.

So how have these new general solicitation procedures fared in practice?

By my estimation the general solicitation provisions, not unexpectedly, got off to a slow start, but data garnered from SEC Form D filings and industry data provider Crowdnetic indicate that this new private placement option is slowly but steadily gaining in acceptance. Old business models, relying on pre-existing investor relationships and self-certification of an investor’s accreditation, remain in tact. However, new technology driven, marketing savvy players have entered the marketplace, notably Internet investment portals, where companies in search of capital are now able to cast a wider net. Deal sizes for non-real estate deals range from the hundreds of thousands to $5 million or more, with real estate transactions reaching loftier heights. However, most deals tend to cap out at the $2 million mark. Though these new platforms are still faced with the reality that deals do not sell themselves, regardless of how broadly they are exposed, greater exposure to potential investors has nonetheless had a measurable benefit to many early stage companies.

By my estimation the general solicitation provisions, not unexpectedly, got off to a slow start, but data garnered from SEC Form D filings and industry data provider Crowdnetic indicate that this new private placement option is slowly but steadily gaining in acceptance. Old business models, relying on pre-existing investor relationships and self-certification of an investor’s accreditation, remain in tact. However, new technology driven, marketing savvy players have entered the marketplace, notably Internet investment portals, where companies in search of capital are now able to cast a wider net. Deal sizes for non-real estate deals range from the hundreds of thousands to $5 million or more, with real estate transactions reaching loftier heights. However, most deals tend to cap out at the $2 million mark. Though these new platforms are still faced with the reality that deals do not sell themselves, regardless of how broadly they are exposed, greater exposure to potential investors has nonetheless had a measurable benefit to many early stage companies.

I believe we will continue to see slow, but steady growth in these platforms’ utility. And very soon I expect that those portals which register as broker-dealers will expand both their revenue and investor base when Regulation A+ comes on line later this year and these portals develop alliances with other broker-dealer networks. And if money invested into these new platforms by investors betting on the financial success of the platforms themselves is any indicator of their future potential, one may expect that many investment portals have a bright future ahead. Witness portals closing out their own raises in the past year or so: names such as CircleUp, CrowdFunder, SeedInvest, Fundrise Realty Mogul and most recently, Patch of Land, to name but a few – at attractive valuations.

Unfinished Business – Title III (Unaccredited Crowdfunding) and Title IV (Regulation A+)

Title III Crowdfunding

Title III – What started out as a bold vision in the form of legislation introduced by Congressman Patrick McHenry in 2011 was interrupted (and disrupted) by Senate amendments, largely at the hands of state regulatory trade group North American Securities Administrators Association (NASAA) and a host of consumer protection groups, in theory to add layers of investor protection, such as FINRA regulated intermediaries, and extensive and ongoing oversized disclosure – a burden which could least be afforded by the community intended to benefit most: startups and very early stage companies, typically with little or no revenue – or resources. The details were left to be worked out by the SEC in the rulemaking process – still not completed.

Title III – What started out as a bold vision in the form of legislation introduced by Congressman Patrick McHenry in 2011 was interrupted (and disrupted) by Senate amendments, largely at the hands of state regulatory trade group North American Securities Administrators Association (NASAA) and a host of consumer protection groups, in theory to add layers of investor protection, such as FINRA regulated intermediaries, and extensive and ongoing oversized disclosure – a burden which could least be afforded by the community intended to benefit most: startups and very early stage companies, typically with little or no revenue – or resources. The details were left to be worked out by the SEC in the rulemaking process – still not completed.

Though the proposed rules were lengthy, the SEC seemed to ask all the right questions, and even added some laudable features enhancing transparency, they were burdened by a defective statutory framework, and in my opinion, further complicated by improvident rulemaking decisions – a subject I covered in an article published in January 2014.

So What Is The State Of The Playing Field Today For Title III Crowdfunding?

According to internationally renowned crowdfunding oracle Richard Swart in remarks delivered last week to a crowdfunding conference in Mountain View, California – Title III of the JOBS Act is officially “dead.” And it is likely no coincidence that his remarks came one day after he attended a private crowdfunding roundtable in San Francisco with SEC Commissioner Kara Stein.

According to internationally renowned crowdfunding oracle Richard Swart in remarks delivered last week to a crowdfunding conference in Mountain View, California – Title III of the JOBS Act is officially “dead.” And it is likely no coincidence that his remarks came one day after he attended a private crowdfunding roundtable in San Francisco with SEC Commissioner Kara Stein.

This is the closest that the crowdfunding community can expect to come to hear that the SEC has in effect, thrown in the towel – not in dereliction of its Congressionally mandated rulemaking functions, but rather in recognition of two realities: Title III leaves much to be desired, and with a shift in power in Congress it is more than likely that legislation will not only be introduced this spring – but passed by Congress and signed into law by this summer. Though the exact details of this new legislation are being worked out behind the scenes, it is expected to bear a striking resemblance to the bill introduced by Congressman McHenry last spring, undoubtedly with  a few modifications and bells and whistles to guard against it getting bogged down yet a second time at the SEC. Expect higher dollar limits ($5+ million), reduced disclosure requirements – especially the need for audited or reviewed financial statements for smaller raises – and the ability to crowdfund without an intermediary – FINRA regulated or otherwise.

a few modifications and bells and whistles to guard against it getting bogged down yet a second time at the SEC. Expect higher dollar limits ($5+ million), reduced disclosure requirements – especially the need for audited or reviewed financial statements for smaller raises – and the ability to crowdfund without an intermediary – FINRA regulated or otherwise.

The biggest unknown – what will this new legislation look like after it passes through the various House and Senate committees, with intense lobbying pressure from NASAA and others? Two things are different this time around the Beltway. First and foremost, Republicans have a greater voice in the Senate; and second, there is the track record of Title III itself: After acceding to the wishes of NASAA et al, the end product was a statute that by any measure was simply unworkable. There is no percentage, political or otherwise, in making the same mistakes twice in a bill aimed at job creation. Moreover, our more forward leaning brothers in the UK have already shown the way with a crowdfunding regime that is both regulated and successful. By most measures the UK crowdfunding market is becoming an important part of small business capital formation landscape – demonstrating that smart, limited regulation will effectively solve most ills. And there is one more intangible to throw in the mix – in the past few months Congressman McHenry, the staunchest Congressional supporter of crowdfunding legislation, has been elevated to Deputy Whip in the House of Representatives and Vice-Chair of the House Financial Services Committee.

Bottom line, for those who have lost patience, and perhaps even interest, expect Title III to get back on track in Congress – a more productive one at that. No, it will not be perfect the second time around, but I expect it will be a starting point, and a good one at that.

Title IV – Regulation A+

As I aptly noted in a prior article, Title IV, now dubbed Regulation A+ by many, might fairly be characterized as the “sleeping giant” of both the JOBS Act and SME finance. It bears little resemblance to its older and largely neglected brother – Regulation A – both little known and little used. This new financing avenue has slowly but steadily received increasing attention and interest from market stakeholders over the past year. What some have dubbed the Mini-IPO, or what I often think of in endearing terms as the “Poor Man’s IPO,” is intended to allow a company to raise up to $50 million per year (eventually even more) in an SEC registered and reviewed offering. It has, as some of its hallmarks, shares which are freely tradable shares upon their issuance, lighter financial and non-financial offering disclosure compared to a full on IPO, and ongoing reporting requirements which are reduced both in terms of the quantity of information and the frequency of ongoing reports.

It is the immediate liquidity and greater transparency which sets Regulation A+ apart from that SEC-exempt capital formation giant – Regulation D and Rule 506 – with no mandatory disclosure, no dollar limitation and a holding period of one year.

And one of the lynchpin’s of Rule 506’s success, federal preemption from state blue sky review, is the necessary ingredient provided by Title IV of the JOBS Act for exchange listed securities and securities sold to “qualified purchasers” – the task of defining who is a qualified purchaser being left by Congress to SEC rulemaking.

Figuring out exactly who ought to be a qualified purchaser, the key to freedom from duplicative state-by-state review, each with its own investor protection requirements, has set off a battle royale, primarily between state regulators, led by their trade organization NASAA, and the Commission. This battle has played itself out with vigor since the SEC promulgated proposed rules in December 2013, and the battle has continued unabated even after the formal closing of the SEC rulemaking comment period.

Figuring out exactly who ought to be a qualified purchaser, the key to freedom from duplicative state-by-state review, each with its own investor protection requirements, has set off a battle royale, primarily between state regulators, led by their trade organization NASAA, and the Commission. This battle has played itself out with vigor since the SEC promulgated proposed rules in December 2013, and the battle has continued unabated even after the formal closing of the SEC rulemaking comment period.

Clearly this is a fight which is heavily stacked against the state regulators. They started with a proposed SEC rule which broadly pre-empted all purchasers as qualified purchasers, so long as their purchases were limited to 10% of their income or net worth. Clearly at least a majority of the Commissioners understood that absent participation in this market by both accredited and unaccredited investors, coupled with 50 state blue sky preemption, this market would never gain traction.

And logic and common sense were also against the opponents of 50 state blue sky pre-emption. NASAA starts from the premise that state regulators can (and will) do a better job of reviewing companies than the SEC – a position not likely to endear itself to the Title IV rulemakers at 100 “F” Street. And then, NASAA is further tasked with the challenge of explaining why a single SEC review suffices for large companies, but both SEC review and state review are required – particularly from smaller companies who can least afford the expense, delay and uncertainty attendant to duplicative reviews.

And logic and common sense were also against the opponents of 50 state blue sky pre-emption. NASAA starts from the premise that state regulators can (and will) do a better job of reviewing companies than the SEC – a position not likely to endear itself to the Title IV rulemakers at 100 “F” Street. And then, NASAA is further tasked with the challenge of explaining why a single SEC review suffices for large companies, but both SEC review and state review are required – particularly from smaller companies who can least afford the expense, delay and uncertainty attendant to duplicative reviews.

But alas, nothing is easy in Washington, D.C. – there are (too) many voices to be heard – and backs to scratch – something that has made the DC metropolitan area this country’s one of the biggest economic bright spots, both during and after the great recession. Logic and good intentions alone are no match for the political forces afoot in Washington.

So Where Are We Today On Regulation A+?

According to a variety of informed sources, I am pleased to report that the Commission is in the final stages of its deliberative rulemaking process. Many, including myself, are hopeful that we will see final rules approved before the 2015 summer solstice. And though no one outside the Commission is privy to the precise details of the final rules, there is strong expectation that the final rules will be workable (as in broad blue sky pre-emption) and are not expected to stray far from the rules as proposed.

We saw signs that the Commission is in the home stretch of Regulation A+ rulemaking – in the form of the agenda of last week’s meeting of the SEC’s Advisory Committee on Small and Emerging Companies (the SME Committee). Until last December this Committee had, inexplicably, failed to meet for 15 months since Chair White took over the reins at the Commission, something I pointed to with concern in an earlier article. Significant is the fact that this Committee was created by Chair White’s predecessor, in 2011, essentially as a sounding board for the Chair on issues deemed of importance to capital formation by SME’s, and the agenda is controlled by the Chair.

So last week’s agenda came as a most welcome surprise. The first item of new business on the agenda was a discussion of the issue of federal pre-emption of state review authority for companies issuing securities under proposed Regulation A+. Predictably, the consensus of the Committee was that state review of SEC reviewed Regulation A+ offerings would be duplicative, adding little to investor protection, but adding a great deal of otherwise unnecessary time, expense and uncertainty to a proposed capital raise. Commissioner Gallagher, a vocal supporter of Regulation A+, added a much needed and welcome comment to the Committee’s deliberative process – when he openly uttered the “m” word – “m” as in merit review.

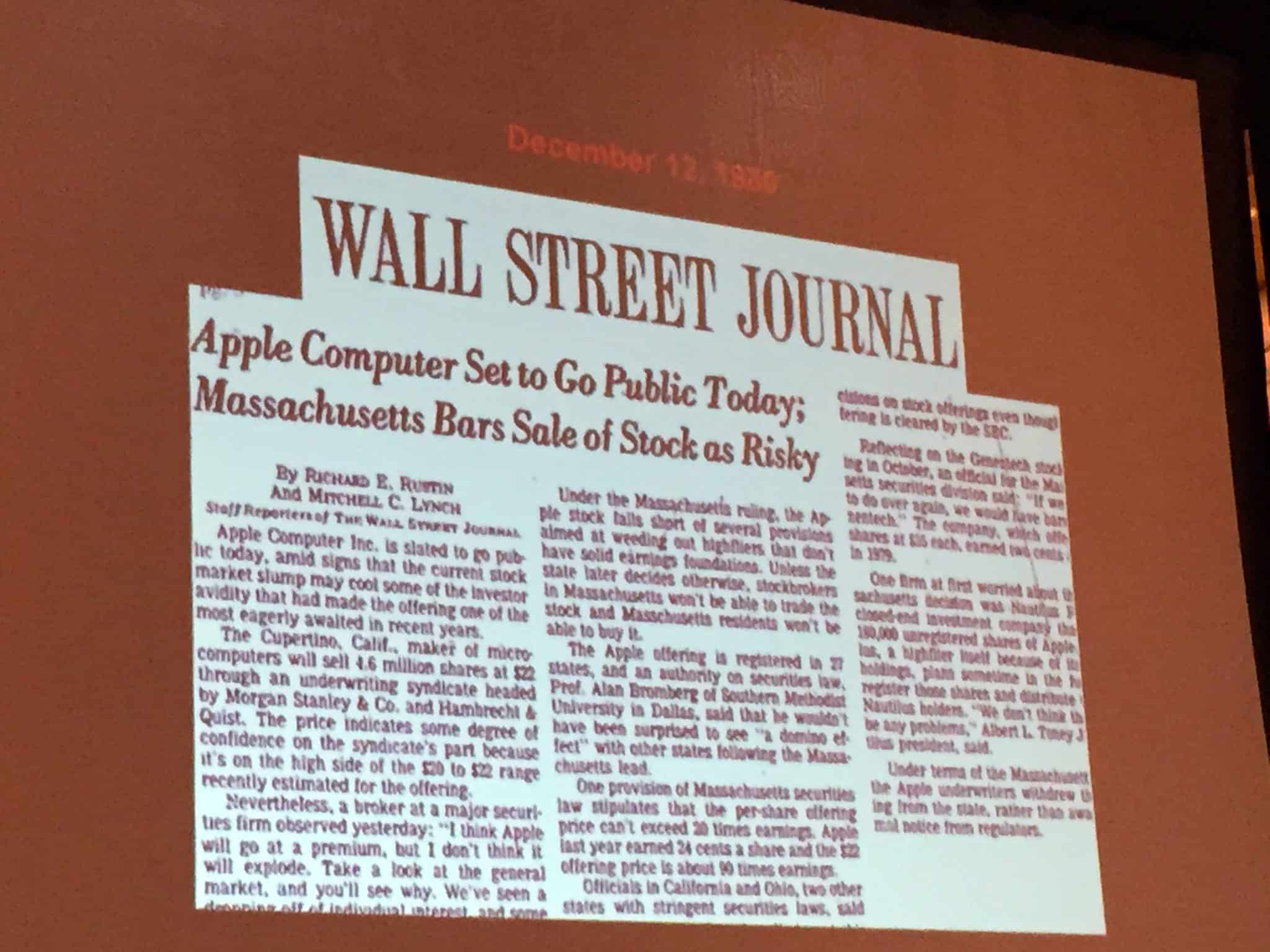

You see, even if all 50 states could guarantee a speedy state review of a Regulation A+ offering, as their new coordinated review system is designed to accomplish, Gallagher pointed out that embedded in the state review process are the varying standards of the 50 states, a significant number of which review the merits of the offering. This standard, often expressed under the statutory mantra of “fair, just and equitable,” means that a state regulator can bar an issuer from selling securities in its state if the offering is deemed too risky for ordinary investors. Witness the decision of the Commonwealth of Massachusetts and more than a dozen other states back in 1980 to bar Apple Computer’s IPO from being sold to retail investors. In their judgment, the Apple IPO was just another hot IPO which was “overvalued.”

You see, even if all 50 states could guarantee a speedy state review of a Regulation A+ offering, as their new coordinated review system is designed to accomplish, Gallagher pointed out that embedded in the state review process are the varying standards of the 50 states, a significant number of which review the merits of the offering. This standard, often expressed under the statutory mantra of “fair, just and equitable,” means that a state regulator can bar an issuer from selling securities in its state if the offering is deemed too risky for ordinary investors. Witness the decision of the Commonwealth of Massachusetts and more than a dozen other states back in 1980 to bar Apple Computer’s IPO from being sold to retail investors. In their judgment, the Apple IPO was just another hot IPO which was “overvalued.”

Case Closed!

So in my estimation the inclusion by the SEC Chair on the SME Committee Agenda of the most contentious issue holding up final Regulation A+ rules, federal pre-emption of state blue sky review – its approval by the SME Committee nothing short of a foregone conclusion – was most likely in the nature of “political cover” for those Washington Democrats who will have to deal with the political fallout from state regulators, consumer groups and their lobbyists the morning after final rules are adopted by the Commission.

So in my estimation the inclusion by the SEC Chair on the SME Committee Agenda of the most contentious issue holding up final Regulation A+ rules, federal pre-emption of state blue sky review – its approval by the SME Committee nothing short of a foregone conclusion – was most likely in the nature of “political cover” for those Washington Democrats who will have to deal with the political fallout from state regulators, consumer groups and their lobbyists the morning after final rules are adopted by the Commission.

Sources close to the final rulemaking process echo the expectation that final rules will be upon us in 60-90 days. Though the exact details will not be known until the Commission formally convenes to vote on final rules, the expectation is that the final rules will be “user friendly.”

The Next Big Headline for SME’S in 2015? Venture Exchanges for Smaller Cap Companies!

From my perspective, all of the latest JOBS Act developments are extremely positive, and will bode well for SME’s – not to mention the U.S. economy. But the big headline out of Washington last week had its origins in Chair White’s preliminary remarks addressing the SME Committee. Though her words were brief, she highlighted the fact that freely tradable securities would be the immediate byproduct of Regulation A+ offerings – and these securities would benefit from a vibrant secondary market. So too for those securities issued in private placements under SEC Rule 506 – which generally are freely tradable after a one year holding period.

From my perspective, all of the latest JOBS Act developments are extremely positive, and will bode well for SME’s – not to mention the U.S. economy. But the big headline out of Washington last week had its origins in Chair White’s preliminary remarks addressing the SME Committee. Though her words were brief, she highlighted the fact that freely tradable securities would be the immediate byproduct of Regulation A+ offerings – and these securities would benefit from a vibrant secondary market. So too for those securities issued in private placements under SEC Rule 506 – which generally are freely tradable after a one year holding period.

The Chair’s proposed solution for the Committee to consider: venture exchanges. In essence, this may be characterized as a secondary market a notch below the current national markets, but with right sized corporate governance requirements and trading rules better suited to the less liquid, smaller cap companies, together with lighter reporting requirements intended to mesh with the proposed disclosure requirements of Regulation A+.

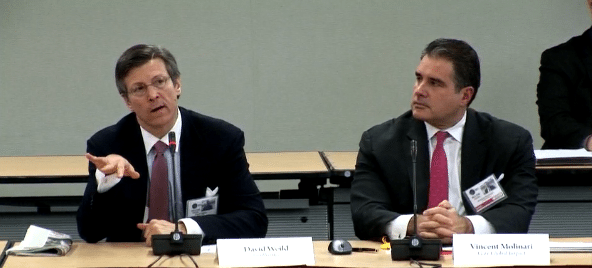

And the central focus of the Committee’s all day meeting: a presentation by former NASDAQ Vice Chairman David Weild, dubbed by many the “Father of the JOBS Act,” on venture exchanges. He outlined in convincing fashion the decline of smaller IPO’s since the 1990’s and the role that secondary trading flaws had played in this decline. According to Weild, some of these flaws were a by-product of well-intentioned SEC regulations implemented in the 1990’s – appropriate for large cap companies – but a show stopper for micro cap and nano cap issuers.

And the central focus of the Committee’s all day meeting: a presentation by former NASDAQ Vice Chairman David Weild, dubbed by many the “Father of the JOBS Act,” on venture exchanges. He outlined in convincing fashion the decline of smaller IPO’s since the 1990’s and the role that secondary trading flaws had played in this decline. According to Weild, some of these flaws were a by-product of well-intentioned SEC regulations implemented in the 1990’s – appropriate for large cap companies – but a show stopper for micro cap and nano cap issuers.

Some bottom lines

There appears to be a decided shift in focus by the SEC Chair and the Commission to addressing the needs of SME’s. Not only has the SEC’s SME Advisory Committee come out of hibernation after 15 months of inactivity, but there are strong indicators that these issues are becoming a priority. Yes, Dodd-Frank rulemaking fatigue may finally have set in at the Commission level – with SME’s being the beneficiary. And not lost on the politically astute commissioners, with Congress now  controlled by the Republicans – there is a new weapon – with edges on both sides. With Harry Reid and other Democrats no longer blocking the introduction of Senate bills, what the Commission is unable or unwilling to do – as far as implementation of the JOBS Act – Congress is standing ready to complete the task. And on the other side, for fresh new ideas for SME capital formation supported by the Commission which require further legislation, there is a willing partner in the form of a Republican Congress – and a new window of opportunity.

controlled by the Republicans – there is a new weapon – with edges on both sides. With Harry Reid and other Democrats no longer blocking the introduction of Senate bills, what the Commission is unable or unwilling to do – as far as implementation of the JOBS Act – Congress is standing ready to complete the task. And on the other side, for fresh new ideas for SME capital formation supported by the Commission which require further legislation, there is a willing partner in the form of a Republican Congress – and a new window of opportunity.

A decision at the SEC Chair level to focus on major new, forward looking areas, such as venture exchanges is not to be taken lightly. And this was followed by an address by Commissioner Kara Stein at Stanford Law School the next day. The focus of her remarks: ongoing SEC JOBS Act rulemaking impacting SME’s – and new, uncharted roads – venture exchanges. And this week, the Senate Banking Committee convened a hearing for the sole purpose of considering venture exchanges – the witnesses being the heads of Nasdaq, the NYSE and the SEC’s Division of Trading and Markets.

So don’t be surprised to see proposed legislation creating the framework for regulatory exchanges to be introduced in Congress this spring. With Regulation A+ upon us, and with both the interest and support of the SEC Chair and other members of the Commission, there  is a very strong possibility, if not likelihood, that legislation clearing a path for new venture exchange may become law by this summer – a move that would inure to the benefit of Regulation A+ issuers.

is a very strong possibility, if not likelihood, that legislation clearing a path for new venture exchange may become law by this summer – a move that would inure to the benefit of Regulation A+ issuers.

So for those of you who care about seeing new, effective avenues of capital formation for SME’s – don’t reach for the champagne bottle quite yet. But it’s not too early to check your inventory.

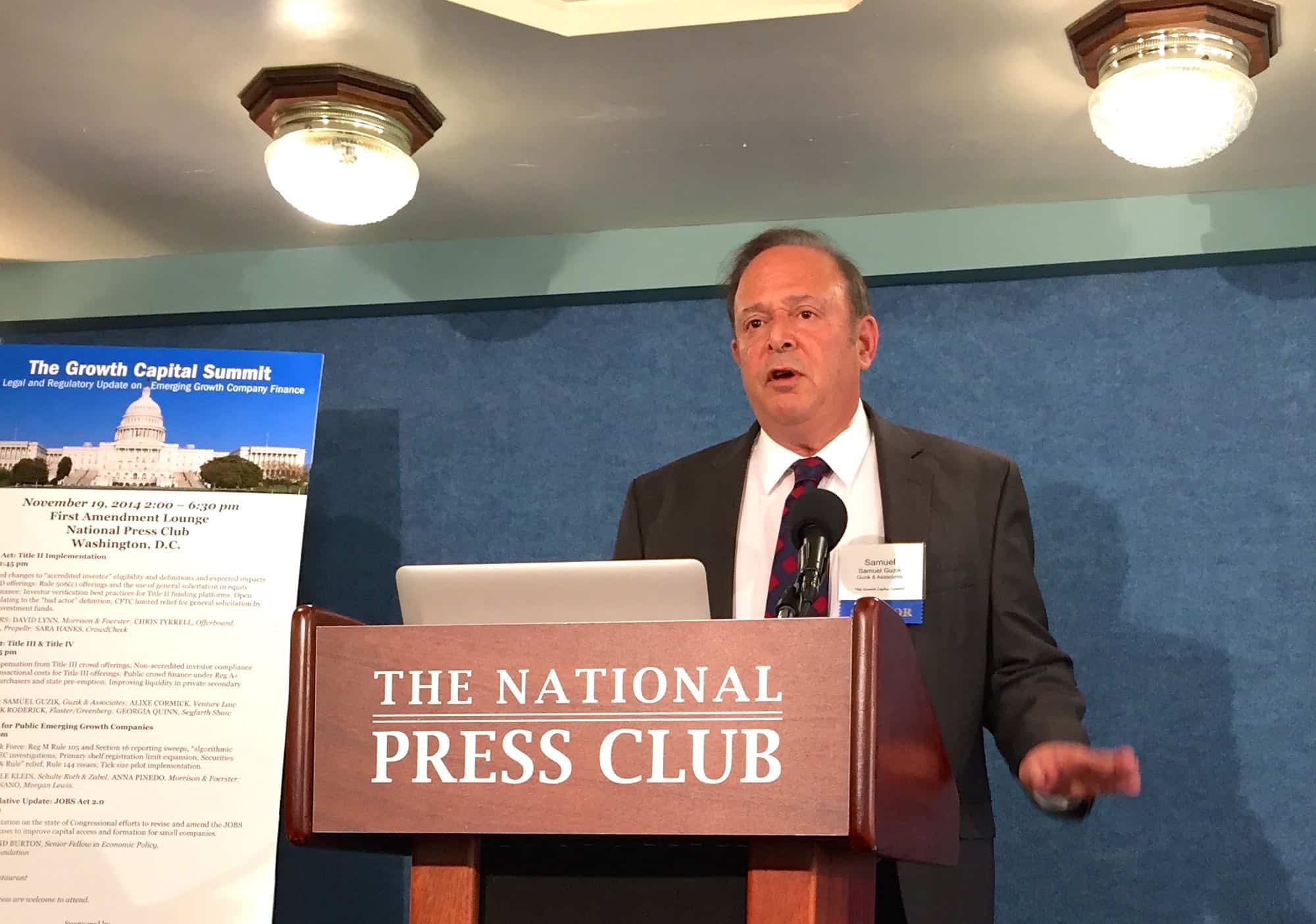

(Editors Note: readers interested in hearing more about the status of Regulation A+ and the future of venture exchanges, you may want to tune into a free Webinar moderated by Dara Albright on Thursday, March 12, 1:30 EDT, and featuring former Nasdaq Chairman David Weild and Senior Contributor Samuel Guzik)

Samuel S. Guzik, a Senior Contributor to Crowdfund Insider, is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience in private practice. A nationally recognized authority on the JOBS Act, including Regulation D private placements, investment crowdfunding and Regulation A+, he is and an advisor to legislators, researchers and private businesses, including crowdfunding issuers, service providers and platforms, on matters relating to the JOBS Act. As an advocate for small and medium sized business he has engaged with major stakeholders in the ongoing post-JOBS Act reform, including legislators, industry advocates and federal and state securities regulators. In 2014, some of his speaking engagements have included leading a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy, a panelist at the MIT Sloan School of Business 2014 Crowdfunding Roundtable, and a panelist at a national bar association event which included private practitioners, investor advocates and officials of NASAA. His articles on JOBS Act issues, including two published in the Harvard Law School Forum on Corporate Governance and Financial Regulation, have also served as a basis for post-JOBS Act proposed legislation. Recently he was cited by SEC Commissioner Daniel M. Gallagher in a public address for his advocacy on SEC regulatory reform for small business. He is admitted to practice before the SEC and in New York and California. Guzik has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.

Samuel S. Guzik, a Senior Contributor to Crowdfund Insider, is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience in private practice. A nationally recognized authority on the JOBS Act, including Regulation D private placements, investment crowdfunding and Regulation A+, he is and an advisor to legislators, researchers and private businesses, including crowdfunding issuers, service providers and platforms, on matters relating to the JOBS Act. As an advocate for small and medium sized business he has engaged with major stakeholders in the ongoing post-JOBS Act reform, including legislators, industry advocates and federal and state securities regulators. In 2014, some of his speaking engagements have included leading a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy, a panelist at the MIT Sloan School of Business 2014 Crowdfunding Roundtable, and a panelist at a national bar association event which included private practitioners, investor advocates and officials of NASAA. His articles on JOBS Act issues, including two published in the Harvard Law School Forum on Corporate Governance and Financial Regulation, have also served as a basis for post-JOBS Act proposed legislation. Recently he was cited by SEC Commissioner Daniel M. Gallagher in a public address for his advocacy on SEC regulatory reform for small business. He is admitted to practice before the SEC and in New York and California. Guzik has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.