[As published on October 28, 2015 in Crowdfund Insider]

I will not be discouraged by failure; I will not be elated by success.”

Joseph B. Lightfoot

The bigger than life headline yesterday? The long-awaited news that the SEC’s five Commissioners would be convening this coming Friday to vote on, and presumably approve final Title III rules. Yet as we wait with great anticipation to see what the final rules will actually say, I wanted to throw out some thoughts to the crowd – thoughts which I and a growing number of others believe are important.

First, a heartfelt thanks, along with my sympathies, to the Staff at the SEC who despite the media headlines to the contrary have worked tirelessly on the Title III rules to get to this day. Not an easy task to build out an entirely new capital formation ecosystem which brings together the riskiest of companies and the most financially vulnerable investors. And to make the task that much more difficult, Congress left much, if not most, of the important details to the SEC. And if that were not enough, the Staff at the SEC was saddled with a statutory structure which was not a product of rational legislative deliberation, but instead the final work product of some very ugly and partisan sausage making on the Senate side of Capitol Hill before Congressman Patrick McHenry’s original House bill would make it to the legislative finish line in April 2012

First, a heartfelt thanks, along with my sympathies, to the Staff at the SEC who despite the media headlines to the contrary have worked tirelessly on the Title III rules to get to this day. Not an easy task to build out an entirely new capital formation ecosystem which brings together the riskiest of companies and the most financially vulnerable investors. And to make the task that much more difficult, Congress left much, if not most, of the important details to the SEC. And if that were not enough, the Staff at the SEC was saddled with a statutory structure which was not a product of rational legislative deliberation, but instead the final work product of some very ugly and partisan sausage making on the Senate side of Capitol Hill before Congressman Patrick McHenry’s original House bill would make it to the legislative finish line in April 2012

And I would be remiss in not giving a special thanks to Sebastian Gomez Abero, Chief of the SEC Office of Small Business Policy, who had the herculean task of wrestling with all of the fine details, and assimilating the many views of those inside the walls of the SEC, not to mention the hundreds of persons who took the time to provide the SEC with their brain share in the form of written comments on the proposed rules and meeting personally with the Staff.

And I would be remiss in not giving a special thanks to Sebastian Gomez Abero, Chief of the SEC Office of Small Business Policy, who had the herculean task of wrestling with all of the fine details, and assimilating the many views of those inside the walls of the SEC, not to mention the hundreds of persons who took the time to provide the SEC with their brain share in the form of written comments on the proposed rules and meeting personally with the Staff.

But alas, let us not lose perspective – Friday will come and go, like any other day. And regardless of what the final rules say, there will be much important work left to be done. So the question du jour is how will this work will get done? And how quickly?

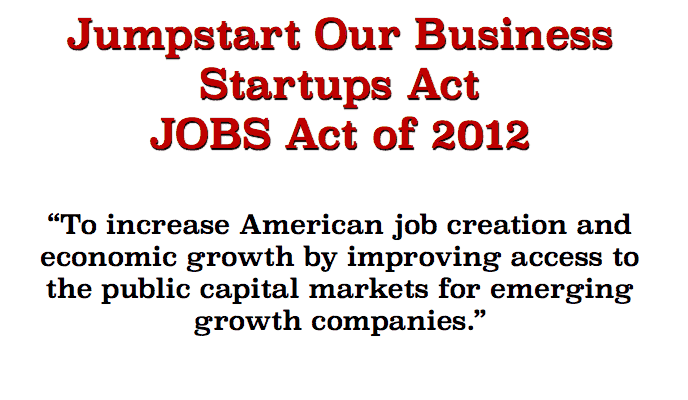

To answer this question properly, one needs, as their starting point, not the 270-day deadline for Title III rules, set by Congress back in April 2012. Actually, I go back a lot further – 1980 to be exact – to remind everyone that long before the bipartisan JOBS Act of 2012 became part of the legislative landscape, Democrats and Republicans alike came together back in 1980 to forge important legislation with a singular purpose – to strengthen the interests of small and emerging businesses in the legislative and regulatory process. These were to be important reforms for SME’s, some of which included:

To answer this question properly, one needs, as their starting point, not the 270-day deadline for Title III rules, set by Congress back in April 2012. Actually, I go back a lot further – 1980 to be exact – to remind everyone that long before the bipartisan JOBS Act of 2012 became part of the legislative landscape, Democrats and Republicans alike came together back in 1980 to forge important legislation with a singular purpose – to strengthen the interests of small and emerging businesses in the legislative and regulatory process. These were to be important reforms for SME’s, some of which included:

- Protection of the interests of small business from unduly burdensome requirements in the federal regulatory process (the Regulatory Flexibility Act of 1980)

- Creation of an annual SEC Government Small Business Forum, to provide a sharper focus on issues directly impacting small business at the SEC and to facilitate communication and cooperation between the SEC, state regulatory agencies, and the other stakeholders in the SME ecosystem.

Though these were important steps, the promise of these measures and measures of similar ilk over the past few decades have not really moved the needle very much – given the amount of time elapsed. In fact, I believe it is fair to say that since 1980 it has pretty much-been business as usual for small business interests in Washington – still lacking strong, effective advocates, both at the SEC and in the halls of Congress.

That is not my opinion alone. Indeed, it would be challenging to find well-grounded opinions to the contrary.

So What is Needed? The Missing Title VIII of the JOBS Act: Creation of a Strong Independent Voice at the SEC – Small Business Advocate.

Well, when it comes to my views on how to ease legislative and regulatory burdens on small business, I first spoke to this issue back in February 2014, in an article first published in Crowdfund Insider: an independent office at the SEC – one whose sole mission was to advocate for the interests of small business capital formation – and with the gravitas to actually have a chance to make a difference. Something more was needed than simply an office in the SEC, dedicated to small business, which has a line of authority on the SEC organizational chart which ends with the Director of the Division of Corporation Finance. What was needed was a strong and independent voice, one that reported directly to not only the full Commission but also to Congress.

To me, the need for this new office at the SEC was obvious. Yet I could find nothing in the public literature discussing this idea before I first advocated for it in February 2014. So in the absence of any prior authority on the subject I questioned: was this was really a good idea; would it really make a difference for small business? Or would such a new office perhaps do more harm than good, as some might postulate. Who would know better the answer to this question than now former SEC Commissioner Daniel M. Gallagher, I thought. After all, he was not only a sitting SEC Commissioner who was a staunch supporter of small business but one who had headed up the SEC’s Division of Trading and Markets, amongst other SEC Staff positions, in a former life.

To me, the need for this new office at the SEC was obvious. Yet I could find nothing in the public literature discussing this idea before I first advocated for it in February 2014. So in the absence of any prior authority on the subject I questioned: was this was really a good idea; would it really make a difference for small business? Or would such a new office perhaps do more harm than good, as some might postulate. Who would know better the answer to this question than now former SEC Commissioner Daniel M. Gallagher, I thought. After all, he was not only a sitting SEC Commissioner who was a staunch supporter of small business but one who had headed up the SEC’s Division of Trading and Markets, amongst other SEC Staff positions, in a former life.

Well, I heard Commissioner Gallagher’s answer to my questions in a private meeting with him back in June of 2014. And the public heard his answer in the affirmative in a major address he delivered at The Heritage Foundation in September 2014, aptly titled “What Ever Happened to Promoting Small Business Capital Formation, complete with a shout out to me in a footnote.” You see, from the perspective of Commissioner Gallagher, one of the line items in his personal “to do list” of necessary reforms to enhance the ability of small business to raise capital and to otherwise comply with SEC rules, was to create an entirely new office at the SEC, an Office of Small Business Advocate.

His words proved to be an inspiration for many, including those within the Beltway who are better positioned than most to make things happen. It started with an organization known as the Small Business Investor Alliance. A stone’s throw from the Hill they took the initiative to garner enough support to have legislation introduced into Congress on October 21, 2015. They started out by finding a friend in the offices of Representative John Carney (D-Del) and Representative Sean Duffy (R– Wisc). Also lending support as co-sponsors of the bill – Ander Crenshaw (R-FL), and Mike Quigley (D-IL).

His words proved to be an inspiration for many, including those within the Beltway who are better positioned than most to make things happen. It started with an organization known as the Small Business Investor Alliance. A stone’s throw from the Hill they took the initiative to garner enough support to have legislation introduced into Congress on October 21, 2015. They started out by finding a friend in the offices of Representative John Carney (D-Del) and Representative Sean Duffy (R– Wisc). Also lending support as co-sponsors of the bill – Ander Crenshaw (R-FL), and Mike Quigley (D-IL).

What started with what seemed like one lone voice with what seemed like a good idea soon became a bill, introduced into the House of Representatives on October 21, 2015, with bi-partisan backing of four members of the House of Representatives, and introduced with a letter of support signed onto by major national trade associations:

- Small Business Investor Alliance

- U.S. Chamber of Commerce

- Biotechnology Industry Organization (BIO)

- Small Business & Entrepreneurship Council (SBEC)

- Association for Corporate Growth National Small Business Association

- Crowdfunding Professional Association (CfPA)

- National Venture Capital Association, and

- National Development Council

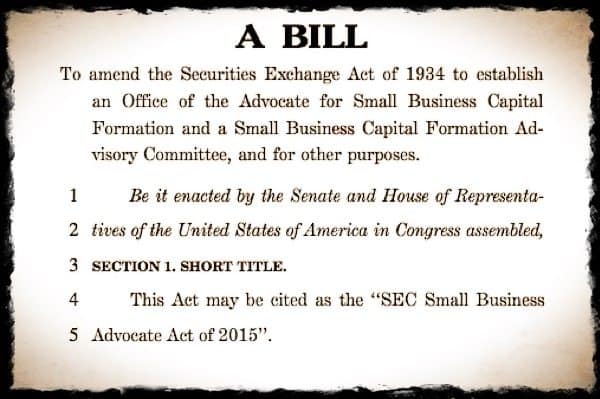

The bill, now officially designated as H.R. 3784, entitled “The SEC Small Business Advocate Act of 2015,” is chocked with details. But suffice it to say that this legislation, which empowers a single individual, the SEC Small Business Advocate, and an office dedicated to the single mission of advocating for promoting capital formation for small business, while also protecting the interests of small business investors, contains the key ingredients. This bill envisions, by legislative fiat, the insertion at the SEC of an individual and an office with a singular focus on small business advocacy, and with the organizational gravitas to get the job done – reporting to the full SEC Commission and to both houses of Congress.

And for those who may think that this legislation is not necessary, all one needs to do is to look at the relatively short shrift that small business has received over the past decades, not to mention the (very) long waits to accomplish tangible reform for small business capital formation. Indeed, the long wait for final Title III rules – long not by my watch, but by Congress’s watch – a 270 day rulemaking deadline mandated by the 2012 JOBS Act itself, pales in comparison when one looks at the small business regulatory landscape going back to the then highly touted small business reforms instituted back in 1980.

So yes, when the jubilation of the crowd in many corners of the U.S. over the long-awaited final Title III crowdfunding rules subsides, let’s pause and take a brief moment to look back a few decades – to learn from history – and then, look not down, but forward. There is much work left to be done to facilitate smarter, right sized regulation of small business capital formation – consistent with necessary investor protections. But we need to work at a more efficient pace then we have over at least the past 35 years.

So after the elation from having final Title III rules subsides, please read this new legislative bill – think about how things might be much different – and better – for small business capital formation if this bill were to become law. Perhaps, the final Title III rules might have been even better than the best efforts of the Staff and the Commission could make them, given that they were already hamstrung by defective legislation passed without the involvement of the Commission. And, perhaps they might have arrived just a tad sooner.

I rest my case.

For a link to the text of H.R. 3784 and the Letter of Support accompanying the bills introduction, it is available for viewing and download here: bit.ly/1P4Jj00 ]